House prices are spiralling out of control, affordable housing is scarce and there are over 478,000 low and very low-income households across Australia in unaffordable rental housing. 100,000 Australians are homeless, 430,000 are on waiting lists for public housing.

This is the result of:

- the absence of a forward-thinking, long term national plan for housing

- a 20-year decline in government investment in social public, and community housing

- Commonwealth rent assistance that has not kept pace with rental increases

- tax laws that favour the wealthy and encourage speculation on ongoing increases in house values

- handouts and subsidies, mostly for first home buyers, that distort and inflate prices

- inadequate prudential standards that encourage buyers to borrow ever-higher sums on low deposits assuming interest rates will remain low

- recent government encouragement for people to use their super to buy homes which pumps up prices while draining super fund accounts.

Our objectives

- Enough new housing to meet Australia’s needs

- Housing that is affordable for renters and home buyers on low to moderate incomes

- Stabilise or reduce house prices

Our plan

- Fund 100,000 new affordable and 100,000 new social and community housing units

- Transfer 50% of public housing stock to community-based housing operators

- Fund safe, permanent and supported housing, no strings attached, for people who have been homeless, medium to long term

- Ensure that 10 percent of the

- Change negative gearing rules to only apply to investment in new housing

- Halve the capital gains tax exemption to discourage speculation on existing housing and long-term house vacancies, currently ~4%

- Discourage investment in housing by self-managed super funds

3. Loan caps

- Introduce sufficient loan caps to prevent real increases in house prices and excessive indebtedness by real estate buyers. A lower cap would apply to investors than first home buyers.

- Develop a long-term national plan for housing

- Reform residential tenancy regulations through the current NHHA to end unfair evictions and tie rent increases to increases in the median wage

Our plan in detail

Investing in 100,000 new affordable and 100,000 new social and community housing units could be funded by the billions saved by limiting negative gearing to new housing and reducing the Capital Gains Tax discount. The Federal Government could borrow at near-zero interest rates which would then be largely recovered by the sale to first home buyers.

Selling the new affordable homes to first home buyers would put downward pressure on all housing prices. A caveat on the property should be added such that it could only be on-sold to other first home buyers for some period of years – but even without that, the new supply of housing would drive down prices.

Adjacent vacant sites or sites with under-utilised low-rise buildings should be aggregated to allow creation of new medium-rise suburbs with schools, cafes, gyms, shops and other amenities.

Actual construction of housing could be delegated to local government. This housing would remain affordable by being relatively compact and have one or no car spaces. New developments should be highly rated “green buildings” with extensive use of solar panels and efficient insulation.

This program would also replace “First Home Buyers” grants that are limited in scope and just push up prices for the limited available housing stock even higher.

The Victorian government has a plan to build 12,000 new homes throughout metro and regional Victoria. Our plan would double or triple the amount of housing that is built in that State.

The ABS Census in 2011 recorded 105,237 people homeless. The causes of homelessness are numerous – lack of affordable housing, poverty, violence against women and children, ended relationships, lack of superannuation in retirement, especially older women, people exiting prison, hospital and out of home care, those affected by addiction and mental illness.

In 2016 the ABS found that 1.26 million Australian women and 370,000 Australian men had, at some point, ended a married or defacto relationship with a partner who had been violent towards them. Many became homeless for a period of time and 24,400 women and 17,500 men were sleeping rough.

Research has shown that it is actually cheaper to house the homeless than to leave them on the streets if all health, law enforcement, tax losses and welfare payments are taken into account.

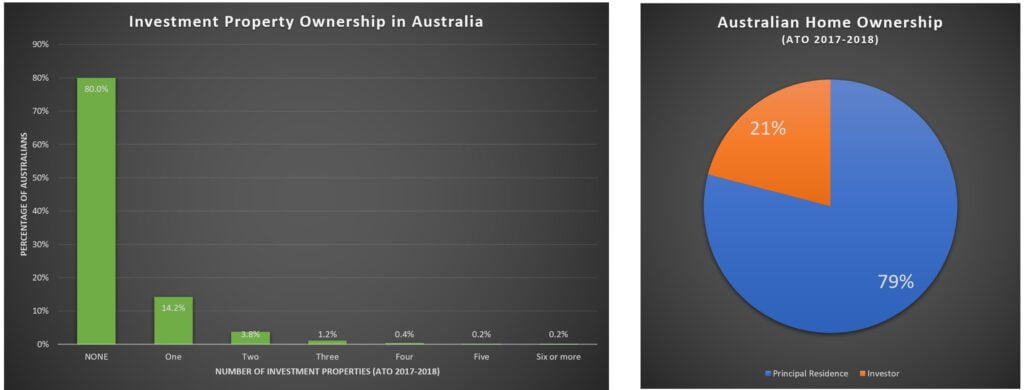

Most of the benefits of the housing tax breaks on housing investment flow to a small cohort of relatively wealthy investors.

The graphs below show that 80% of people do not own an investment property. Less than 5% own more than one investment property. Just over 20% of homes are owned by investors.

Inequitable tax breaks on speculation are costing over $20 billion per annum and driving up housing costs. By comparison an adequate social housing program would probably cost $5 to $10 billion per annum now. (See Australia needs to triple its social housing – The Conversation)

Changing Negative Gearing so it only applies to new housing

Under negative gearing, net rental loss can be used to offset personal income tax. In 2016/17 about 9 percent of taxpayers (or 1.3 million people) reported a net rental loss with an average loss of $8,771. Almost half the benefits went to Australia’s wealthiest 20%. Source: Who really benefits from Negative Gearing? (Australia Institute, 2018)

The total cost of the negative gearing tax break in 2017-18 was over $13 billion. Limiting negative gearing to new housing only will:

- Reduce the ability of investors to out-bid home buyers.

- Allow billions in government funds to be redirected to publicly funded housing projects.

- Direct the remaining negative gearing tax break towards increasing the supply of new houses.

We propose that the negative gearing tax break on existing property be removed at the first budget after the election. Property owners have had this tax break for long enough, its time now to use the funding to assist the people locked out of the housing market instead of wealthy investors.

Reduce the capital gains tax discount to 25%

The CGTC discount in 2018-19 was over $10.6 billion. As part of our fiscal reform platform, we propose to reduce the CGT discount from 50% to 25%. Treasury estimates that the CGT discount cost $10.6 billion in lost revenue in 2018/19 (as stated in Treasury’s Tax Benchmarks and Variations Statement 2020, E15).

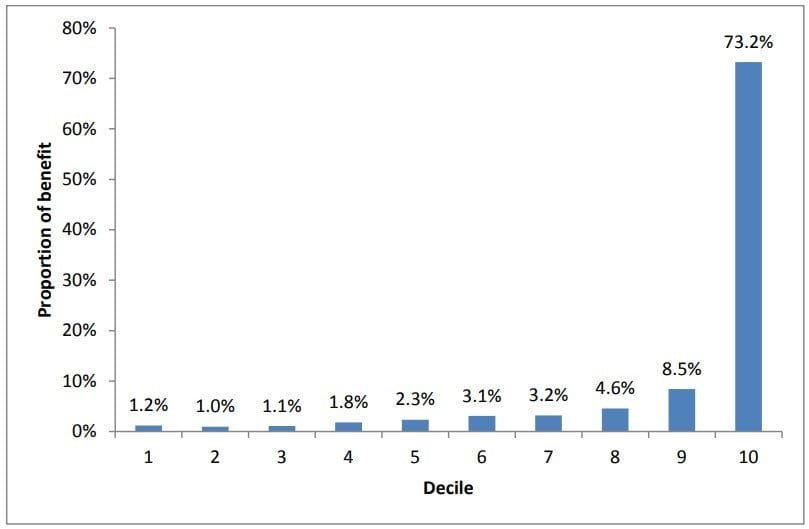

Negative gearing and the CGT discount combine to offer a massive benefit enjoyed chiefly by the top 10% of Australians.

How negative gearing and the capital gains tax discount benefit the top 10 per cent and drive up house prices. (Australia Institute, 2015)

See Reforming the Tax System for more details.

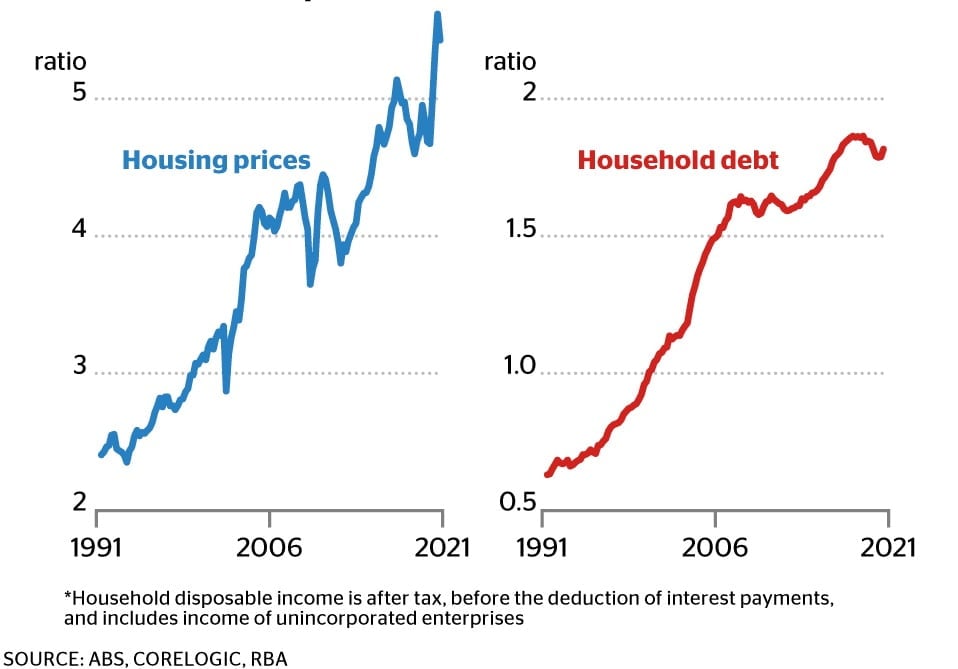

Record low interest has allowed home buyers to borrow huge sums to bid against each other in an over-heated market. This has turned the residential property market into a huge Ponzi scheme and directed finance away from more productive investments.

Loan caps would prevent borrowing for real estate purchases over defined limits with the objective of gradually lowering property prices over time.

Australian Prudential Regulation Authority (APRA) should set tougher loan caps and adjust regularly to achieve the desired goal of lower house prices. The formula used to set the cap could consider:

- If the borrower(s) are first home buyers, movers or investors

- The recent taxable income of the borrowers

- The value of the property

- The properties vulnerability to climate change events

Housing organisations such as the Australian Housing and Urban Research Institute have been calling for a nationally coordinated housing plan that meets housing needs for many years, one that:

- involves all levels of government in planning and delivery

- raises standards of social housing

- ensures suitability for a range of household types

- facilitates supported accommodation for people with disabilities and chronic illness

- decreases concentrations of socially disadvantaged people in public housing

Tenant rights are currently a matter for the states but there are few protections for tenants from unfair evictions and unreasonable rents – another factor in making housing unaffordable. Our plan is for the National Housing and Homelessness Agreement to include a nationally consistent tenants’ rights framework which would mean:

- Evictions must be based on reasonable grounds such as:

- the renter is significantly in breach of their lease, or

- the landlord genuinely needs to move in, or

- the premises are to be extensively renovated or put to a different use , the plans or which are approved by the local authorities,

- Leased property is maintained to at least the standard in which it was let, and meets reasonable safety standards

- Rent would only increase in line with movements in median weekly earnings.

Housing has become less affordable, particularly for young people, partly because of wage stagnation, HECS debt, more casualised, part time jobs.

The ‘marketplace’ tends to build and promote larger houses, many of which are unsuitable for the diverse housing needs of people and their capacity to pay. Energy efficiency standards and tighter planning controls, whilst making housing more sustainable, have up-front higher costs.

Houses have been withdrawn by investors from the rental market for short term holiday operators like Airbnb. Prosper Australia estimates that about 4% of all residential property in Australia – or two years of housing supply – is left vacant. Landowners do this as vacant property is often more valuable to them in the short term if they consider it a speculative asset and holding costs are low. Until supplies of housing are adequate, Federal and State governments could discourage property being left vacant using tax and other means.

Background

Housing is a joint Commonwealth/State responsibility and under the National Housing and Homeless Agreement, established in 2018, $1.6 billion/year is provided by the Federal Government, matched and managed by the states. This level of funding barely keeps up with population increases and falls well short of what’s required to fix the crisis of neglect.

Just $129 million of this annual funding is targeted for homelessness

The current Government’s answer to housing affordability is loan guarantees for 10,000 first home buyers to buy a home on a 5% deposit (rather than 20%) but this will assist less than 10% of first home buyers.

Instead, the urgent need is for community and social housing to be treated as essential infrastructure, much like schools, prisons and hospitals, and funded based on need. The Australian Housing and Urban Research Institute recommends a combination of capital grants and efficient financing and warns that over the next 20 years over 700,000 additional social dwellings will be required.

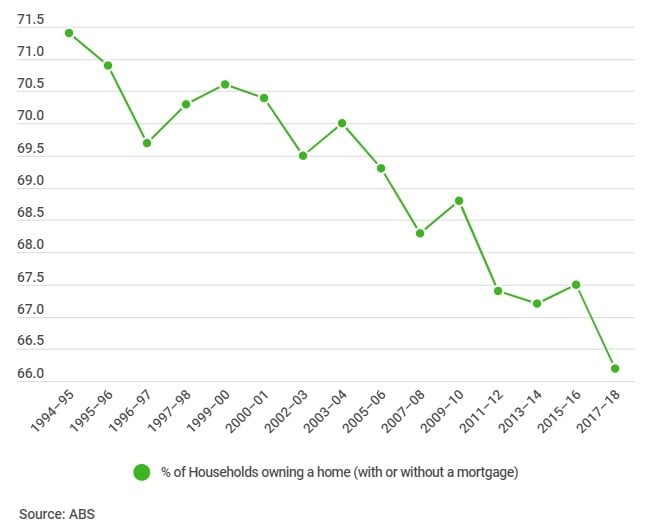

Since 1994-5 the number of households owning their own home has been in steady decline, particularly for under 40-year-olds, due largely to tax breaks that favour investors over home buyers.

References

National Affordable Housing website (A not-for-profit social value enterprise to lobby for more affordable housing options in Australia.)

- National Shelter (A non-government organisation that aims to improve housing access, affordability, appropriateness, safety and security for people on low incomes.)

- Negative gearing cost reaches $13 billion a year (Sydney Morning Herald, 2020)

- Fact check: Did abolishing negative gearing push up rents? (ABC, 2016)

- Australian home ownership & tenancy (Dominic Beattie, Savings.com.au)

- How a millionaire pays no income tax (The Age, 2019)

- If we realised the true cost of homelessness, we’d fix it overnight (The Conversation, Sep 2020)

- Australia needs to triple its social housing by 2036. (The Conversation,2018)

- Who really benefits from negative gearing? (Australia Institute, 2018)

- How negative gearing and the capital gains tax discount benefit the top 10 per cent and drive up house prices. (Australia Institute, 2015)

- Reform of the personal income tax system (ACOSS, 2009 )

- Liberal senator backs redeploying of superannuation early access scheme (The Age, April 2021)

- Sydney and Melbourne house prices rise tens of thousands of dollars in one month (The Age, April 2021)

- Let’s make renting fair (rentingfair.org.au)

- Homelessness and housing (Australian Human Rights Commission)

- Implementation of the National Partnership Agreement on Homelessness (Australian National Audit Office, May 2013)

- Homelessness statistics (Homelessness Australia)

- Housing affordability: Rise of Bank of Mum and Dad fuels inequality in hot market (Domain, April 2021)

- National Plan for Affordable Housing (PDF, Community Housing Industry Association)

- Victoria’s Big Housing Build (Victorian government initiative to build 12,000 homes)

- City of Melbourne Affordable Housing Plan

- AHURI analysis on housing, homelessness and domestic and family violence

- Treasury estimates that the capital gains tax discount cost $10.6 billion in lost revenue in 2018/19 (as stated in Treasury’s Tax Benchmarks and Variations Statement 2020, E15).

- We need a top-level inquiry into runaway home prices – and Ken Henry’s up for it (The Age, August 2021)

- Melbourne houses climb $457 a day amid fears of living standard hit – “Ponzi Scheme” (The Age, September 2021)

- Lending restrictions need to be considered (SMH, September 2021)

- APRA’s moves to cool housing could end banks’ golden run (AFR, April 2021)

- To fix Australia’s housing affordability crisis, negative gearing must go (The Conversation, April 2021)

- Value of macro-prudential reforms such as loan caps (ABC, September 2021)

- Time for a crackdown on ‘liar loans’ to douse home price bonfire (Jessica Irvine, The Age, Oct 2021)

- APRA tightens home loan standards for new customers as risks grow (The Age, Oct 2021)

- How do you raise mortgage rates without actually raising them? (Guardian, Greg Jericho)

- Now it’s Liberals telling us we are going to have to cut the CGT concession (The Conversation, By Peter Martin, Oct 2021)

- One graph that shows why it’s harder for Millennials to buy a house (Elizabeth Redman, The Age, Dec 2021)

- Rate rises may slow housing market but no affordability improvement in sight (The Age, Jan 2022)

- Investor with 8000 homes calls for negative gearing to be axed (The Age, Feb 2022)

- Fairer housing should mean those who have, help those who have not (The Age, Mar 2022)

- ‘It’s all going up’: Workers face rental stress in key marginal seats (The Age, Mar 2022)

- ‘Pure electioneering’: First-home buyer help will increase property prices, experts warn (Domain, Mar 2022)

- Why the rental housing crisis gripping Australia is NOT going to end anytime soon (Daily Mail Australia, Mar 2022)

- ‘Housing in Australia is broken’: only 1.6% of private rentals are affordable for those on minimum wage (Guardian, Apr 2022)

- New policies barely lighten the load when it comes to affording a home (The Age, May 2022)

- Negative gearing and capital gains tax breaks go to top income earners and men (Domain, May 2022)

- ‘I’ve never felt this vulnerable’: Guardian readers share their rental crisis horror stories (Guardian, May 2022)